Your North Shore Oahu Home Just Changed Flood Zones — and Most People Don’t Know Yet

FEMA’s updated flood maps are going into effect on June 10, 2026 and if you own a home on Oahu, they could have a direct impact on your insurance costs, building plans, and property value. If your home has been moved into a high-risk zone, there are a few important changes you need to understand. Here’s what it means for you and how to prepare.

If your home is newly mapped into a high-risk Oahu flood zone (Zone A, AE, VE, etc.) and you have a mortgage, your lender will likely require flood insurance.

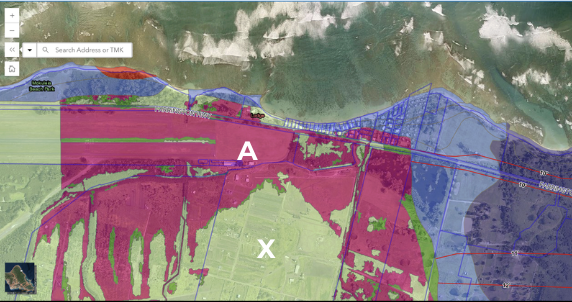

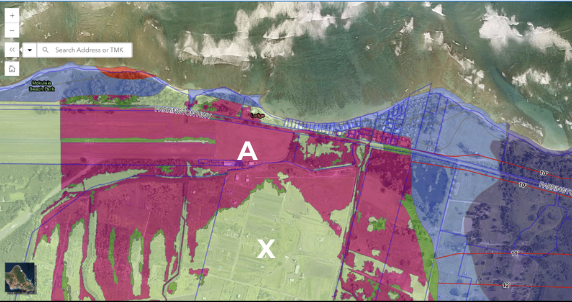

Mokuleia, Before & After Oahu Flood Zone Changes

Impact of Moving from Zone X to Zone A

There are 3 main considerations to keep in mind if your home has moved into an Oahu flood zone:

1. Mandatory Flood Insurance

- If you have a federally backed mortgage (FHA, VA, USDA, or Conventional), your lender will likely require you to carry flood insurance once the maps become official on June 10, 2026.

- The 45-Day Window: Lenders typically send a notice giving you 45 days to provide proof of insurance. If you don’t, they will “force-place” insurance, which is significantly more expensive and provides less coverage than a policy you buy yourself.

- Cost: While Zone X policies are often under $600/year, Zone A policies can be higher. However, you are eligible for the “Newly Mapped” discount. If you buy a policy within the first 12 months of the map change, you can save up to 70% on your initial premium.

2. Stricter Building & Renovation Rules (ROH 21A)

- The 50% Rule: If you plan a renovation that costs more than 50% of the market value of your structure (not the land), you may be forced to bring the entire house up to current flood codes.

- Elevation Requirements: For new builds or substantial improvements in Zone A, the “lowest floor” (including utilities like water heaters and electrical panels) must generally be elevated to at least 1 foot above the Base Flood Elevation (BFE).

- Permit Delays: You will now need a Flood Development Permit for even minor exterior work, which adds a layer of bureaucracy to the standard DPP permitting process.

3. Property Value & Disclosure Requirements

- As a homeowner (and especially if you were to sell), the “Zone A” designation is a material fact.

- Selling: You must disclose this new flood status to potential buyers. While it shouldn’t stop a sale, it increases the “carrying cost” for the next owner due to the insurance premiums, which can affect your total pool of buyers.

- Appraisals: Appraisers will note the high-risk zone, which may slightly impact the valuation if the home isn’t already mitigated (elevated).

Is Your House In a New Oahu Flood Zone?

A great resource is to look it up on your own via: https://www.resilientoahu.org/firm-update. Interested in more Flood Zone details or Oahu Real estate information? Please reach out.

Leave your opinion here. Please be nice. Your Email address will be kept private, this form is secure and we never spam you.