Ask a Lender: Hawaii’s Real Estate Market from a Lender’s Perspective

What a difference a year can make in the real estate market! There is an ongoing discussion about the status of the market and no one really knows what the future holds. Now as things “settle down,” people are feeling more confident about their opportunity to buy, sell or invest in real estate. There are also people with reservations or just want more information before they take action. This year has been full of buzzwords like “historically low rates” and “federal reserve” but how does this impact your goals? Realtors often work collaboratively with lenders to help clients reach their goals. Generally, I can show you what the housing market has to offer and a lender provides your budget. Let’s address commonly asked questions posed by clients. Our local lender, Gregory Turner with Aligned Mortgage, will provide his thoughts on today’s market.

Is it a good time to buy with the “seller’s market” and rising interest rates?

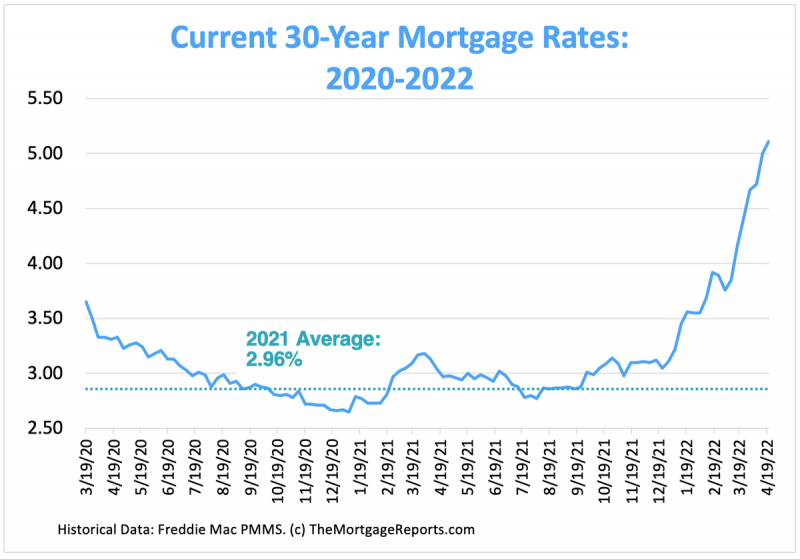

Interest rates are indeed rising, but they are still averaging at a historical low. Low housing inventory, increased rent prices, and affordability are just a few ailments of today’s market. They are emphasized negatively because they all play a part in driving interest rates upward. Mortgage News Daily stated, “the market has not experienced rates this high since 2009 at an average of 5.04%.” It’s still a good time to purchase a home if you have the means i.e. savings, retirement, stocks, etc. and a plan for doing so. Remember renting is always zero return on your investment. For an in-depth view of rates historically, see Federal Home Loan Mortgage Corporation (FHLMC) or Freddie Mac graph. For information on steps you can take to qualify, seek a local mortgage expert.

Why are the interest rates rising?

The rise is a consequence of multiple national economic circumstances. Inflation, COVID-19, and new construction shortage are the main culprits. COVID-19 was a health and economic crisis because it forced the leaders of our nation to spend a lot of money to protect us from economic collapse. You must remember that so many people were not working during the height of the pandemic for so long. Many small businesses that were the backbone of our communities did not survive. A few months ago, the federal government made an announcement stating basically “we spent too much.” We owe more money to other nations, we need to print more money for ourselves, and the value of the money we have is dwindling. The solution was to bounce back quickly: carefully flood the markets by supporting goods, services, labor, and all business sectors, public or private. If they make more, we spend more meaning the public is consuming again.

How do interest rates impact sellers?

In our market today, it’s a great time for a seller to sell their house since there are so few available to buy. Over the past 12 months there has been a 15.5% decrease in the number of active listings on Oahu. However, buyers aren’t too excited about going into a bidding frenzy. They are opting to wait, hoping the rates and prices will decrease in their favor. This is creating a stalemate at the business table where eventually no one eats, or everyone is left unsatisfied and with buyer’s remorse. I recall a story where one buyer paid hundreds of thousands of dollars over the asking price just to avoid losing another bid. This purchase is still ongoing, but that seller will strike gold and other sellers are looking for similar if not better results. What they are not aware of is that they are making an expensive place even more expensive for their predecessors. Some sellers are not this fortunate. Houses are doomed to be sitting on the market for months while buyers search for a more affordable home. Some sellers have lowered prices below the fair market just to attract buyers which excites a bidding frenzy. I advise sellers to get to know your comparable and the value of your neighbors’ houses and what your home is appraised for and start your pricing from there. Get your property surveyed if you haven’t already. And make it easier for your buyer to see the evidence of value in your home. The goal is to move out with your hard-earned equity, not someone else’s hard-earned money, right?

How much do I need for a down payment?

Depends. Down payment is determined by the loan amount, all borrowers’ credit scores, and the different loan programs themselves. It could be 3% down with discount points. It could be 0% down with an income restriction. If you ever served in the military, you could earn enough lender’s credit to pay for all your closing costs. For the best strategy talk to your local mortgage expert to learn about the products you qualify for.

What are closing costs?

An expense that must be paid, usually in a lump sum at closing and signing which includes but is not limited to taxes, title insurance, and attorney’s fees. This is separate from the purchase price and interest.

Why use a mortgage company versus a traditional bank or credit union?

Traditionally, banks, credit unions, and mortgage companies are the same. Each institution has different overlays, but the business model is the same: Lend money from the institution to the borrower directly in good faith, sell the loan on the secondary market, and prevent foreclosure as much as possible. The difference lies in who stands to benefit more in each type of institution, the borrower, or the institution itself. Not all banks, credit unions, or mortgage companies are created equal, so each type has its pros and cons. Banks and credit unions offer the traditional experience you expect. For a more personal experience, go to mortgage companies. If you think the institution with the lowest rates is the best deal, then you did not do enough homework. For first-time homebuyers, I advise you to work with a licensed Mortgage Loan Originator (MLO) regardless of institution. An MLO must protect their institution, but they have a fiduciary duty to borrowers they don’t get paid until the borrower closes. By federal law, you get free mortgage service where you pay only if you are 100% satisfied or your money back guaranteed except upon request of borrower-paid services. Most banks and credit unions only protect the title and the house itself, and will penalize you the moment you default or are late to make payments. Bank only serves the interest of its investors, not the customers or their money. Mortgage companies MLOs will continue to be resourceful to you after you move into your new home. Banks typically will not. Credit unions tend to follow suit except in a “non-profit” way… and that’s through its account holders. Same-same though! But it’s up to you, the consumer. For more legal advice, consult with your CPA or attorney professional.

There are many questions and opinions about the real estate market in Hawaii. Answers vary from island to island. But the most important question still remains “Is this the right time for you to take action in this market?” Get advice on your specific situation and outline your own plan. If you are a buyer, start the conversation with a lender. If you are looking to sell, start a conversation with a real estate agent. A qualified professional will advise you of the options that lead to the best results. Be wary of professionals that are making guarantees or iron-clad predictions about the future of Hawaii’s market. And lastly, be encouraged. There were over 2,500 homes sold from January 2022 to March 2022 and over 2,000 more sales are pending. The market is very active and it may be the best time for you.

Nicky

April 25, 2022

Great blog Ricshara!